| Why is a 555 score so bad? Lenders see it as a red flag, signaling that you might not be the most reliable borrower. This means you’ll likely face higher interest rates and fewer loan options. But don’t worry, there’s hope! One effective way to climb out of this credit hole is to get a secured credit card. Think of it as a safety harness. You’ll need to put down a security deposit, but this shows lenders you’re committed to paying back your loans. By using the card responsibly and paying your bills on time, you’ll start to build a better credit history. |

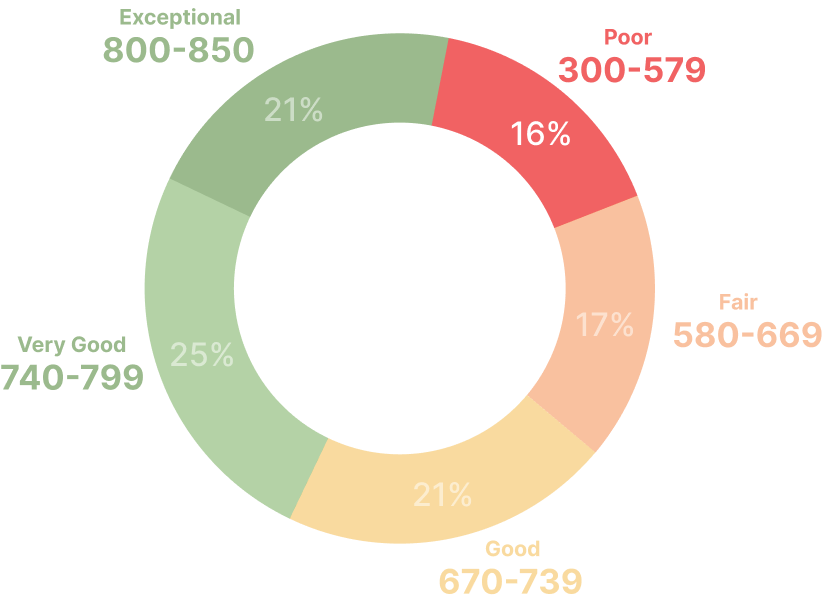

A 555 credit score puts you in the “very poor” range, which means you’ve faced some credit struggles. Lenders see you as a higher risk with a 555 credit score, making it tough to get approved for personal loans, mortgages, or credit cards. Even if you’re approved, you’ll likely face higher interest rates, which increases borrowing costs.

Let’s explore what a 555 credit score means, your chances of qualifying for loans or mortgages, and the steps you can take to improve your score.

| Experian reports that 91% of consumers have FICO® Scores higher than 555. |

How Does a 555 Credit Score Affect You?

A 555 credit score can significantly impact various aspects of your financial life. It not only makes it harder to get approved for loans and credit cards but also affects interest rates, rental applications, and even insurance premiums. Understanding how a 555 credit score influences these areas can help you better navigate your options and take steps to improve your financial situation.

- Tougher Loan and Credit Card Approvals: With a 555 credit score, many lenders see you as risky, making it tough to get approved for personal loans, credit cards, or mortgages. You may encounter more rejections or need a co-signer or collateral to secure approval.

- Higher Costs When Borrowing: If you get approved for credit, you’ll likely face higher interest rates, making borrowing more expensive. You’ll pay more interest over time, and lenders may offer stricter terms, like shorter repayment periods or lower credit limits.

- Impact on Housing, Insurance, and Employment: Your 555 credit score can affect more than just loans. Landlords might deny your rental application, insurers charge higher premiums, and some employers may even check your credit when hiring, especially in certain fields.

Take Control of Your Credit with AI-Powered Insights— Start Repairing Now!

Get StartedCommon Reasons for a Credit Score of 555

Lenders consider a credit score of 555 very poor, often due to several key factors:

- Missed or Late Payments: With a 555 credit score, you’ve likely missed payments or paid bills late. Since payment history is the most important part of your credit score, even a single late payment can have a big impact, signaling to lenders that you may struggle to repay what you owe.

- Short Credit History: If your credit score is 555, it could be because you don’t have a long credit history. The longer you’ve managed credit accounts responsibly, the better it is for your score. With a short or troubled credit history, lenders might not have enough trust in your ability to manage debt, contributing to a lower score.

- Lack of Credit Variety: A 555 score might also indicate that you don’t have a diverse credit mix. Lenders prefer to see that you can handle different types of credit, like credit cards, loans, or mortgages. If you only have one credit type, it might make them doubt your ability to manage different financial obligations.

- Frequent/New Credit Applications: If you’ve applied for multiple new loans or credit cards recently, it could have caused your score to dip to 555. Lenders may see this as a sign that you’re facing financial difficulties or urgently need money, which increases your risk perception and lowers your score.

- Errors on Your Credit Report: Sometimes, a score of 555 can result from mistakes on your credit report. Incorrect information, like a late payment that wasn’t yours or a wrong account balance, can hurt your score. Reviewing your credit report for any mistakes that might be dragging down your score is important.

- High Credit Usage: A 555 score may also suggest that you’re using a large percentage of your available credit. If you’re close to maxing out your credit cards, lenders see this as a red flag, indicating that you might be overly dependent on credit. Keeping your credit usage below 30% of your total credit limit can help improve your score.

| Use CoolCredit to Help Improve a 555 Credit Score One common habit among those with good credit scores is checking their credit reports regularly. You can get a free report from each of the major credit bureaus. In addition to regularly checking your credit report, it’s smart to enroll in credit monitoring services. These services track your finances and notify you if any suspicious activity occurs. With CoolCredit, you’ll have the tools to take control of your credit and start improving that 555 score! |

Steps to Improve a 555 Credit Score

If you have a credit score of 555, there are several steps you can take to start improving it:

Be a Prompt Payer: One of the most effective ways to raise your credit score is to pay your bills on time. Late payments impact your credit, so ensuring you pay everything by the due date will gradually help rebuild your score. Establishing automatic payments or setting reminders can assist you in staying organized.

Be a Prompt Payer: One of the most effective ways to raise your credit score is to pay your bills on time. Late payments impact your credit, so ensuring you pay everything by the due date will gradually help rebuild your score. Establishing automatic payments or setting reminders can assist you in staying organized.

Manage Your Credit Card Debt: High credit card balances can hurt your score because they increase your credit utilization rate, which is how much of your available credit you’re using. Try to pay down your balances as much as possible, ideally keeping your credit usage under 30% of your total credit limit. This will show lenders that you’re managing your credit responsibly.

Hold Off on New Credit: Each time you apply for new credit, it can cause a slight dip in your score. Too many applications in a short time can make you look like a riskier borrower, so it’s best to avoid opening new credit accounts unless it’s necessary. Concentrate on enhancing your current accounts before seeking new credit options.

Dispute Errors on Credit Reports: Mistakes on your credit report can unfairly drag down your score. If you spot an error, such as a late payment that wasn’t yours or an incorrect balance, you should dispute it with the credit bureaus. Correcting these errors can give your score a quick boost. Regularly checking your credit report ensures you catch any mistakes early.

Unlock AI-Powered Credit Solutions— Install the App and Improve Your Score!

Get StartedBoost and Repair: A Simple Path to Build Stronger Credit with CoolCredit

Improving your credit score starts with boosting it, and CoolCredit makes this process simple and effective. Within 30 to 60 days, you can begin to see noticeable improvements. Our AI system reflects new accounts with timely payments on your credit profile by focusing on positive payment reporting. Setting up a Booster Payment plan and making consistent payments, you’re already on your way to a higher score. Plus, CoolCredit lets you boost your score multiple times, providing continuous improvement with our no-interest plans, making it easy to take control of your credit.

Once we boost your credit, we take the next crucial step of repairing it. This involves tackling those negative items on your report that are dragging down your score. CoolCredit’s AI takes a targeted approach, identifying these negative marks and working persistently to remove them. Repairing credit can take time, but our system manages this challenge and continually works to eliminate these items. The goal isn’t just short-term improvement; CoolCredit is here to help you maintain long-term credit health.

Conclusion

A 555 credit score is just the beginning, not the end of the road. With the right actions, you can turn things around and see improvement. It’s all about taking proactive steps—whether setting up a plan to pay down debt, disputing errors on your report, or building positive payment habits. Although you might feel overwhelmed, remember that credit scores change over time, and you have the power to improve yours.

Improving your credit isn’t an overnight process, but you’ll see progress with consistent effort. Little by little, those positive changes will add up, and that 555 score will become a thing of the past. Whether you’re boosting or repairing your credit, know that a higher score is within reach with patience and commitment.

FAQs

Q: Is 555 a Good Credit Score?

A: A 555 credit score isn’t great—it’s considered pretty low. With a score like that, lenders often reject your applications for loans or credit cards, and if they approve you, they’ll likely offer unfavorable interest rates.

Q: Does Diversifying My Credit Mix Help Improve My 555 Credit Score?

A: Absolutely! Adding different types of credit accounts can positively impact your score by demonstrating your ability to manage various forms of credit responsibly. A diverse credit mix shows lenders that you can handle different types of credit, which can boost your overall credit profile.

Q: Can I Buy a House with a 555 Credit Score?

A: Getting a mortgage with a 555 credit score can be challenging, but it’s not impossible. Consider asking a trusted person to co-sign your mortgage to strengthen your application. Offering a larger down payment can also help show lenders you’re serious. Additionally, look into Federal Housing Administration (FHA) loans, as they’re generally more accommodating for those with lower credit scores. With some effort, homeownership can still be within reach.

Q: How Much Can a Credit Score Improve for Someone Beginning at 555?

A: The average rate of credit score improvement can differ from person to person, but, if you practice responsible credit habits, you can often see significant changes within just a few months.

Q: Is It Possible to Obtain an Auto Loan With a 555 Credit Score?

A: Yes, getting an auto loan with a 555 credit score is possible, however, be prepared for higher interest rates. If you’re considering a $30,000 car loan, you could end up paying over $10,000 more in interest compared to someone with a better score. So getting a loan is possible, it’s important to understand the financial implications.

Q: How Can I Improve My 555 Credit Score?

A: If you’re looking at a 555 credit score, it’s important to figure out why it’s below average and take proactive steps to improve it. Begin by frequently reviewing your credit reports from the major credit bureaus. Keep an eye out for errors or inaccuracies, like wrong account details or missed payments that aren’t yours. Disputing these mistakes can help boost your score.

With CoolCredit, you can perform a comprehensive credit analysis, which gives you detailed insights into your credit report. This analysis will pinpoint the areas that need attention and provide actionable steps for improvement, making it easier to raise your credit score. By using these resources and being proactive, you can work toward a healthier credit profile and open up more financial opportunities for yourself.

The post 555 Credit Score: What It Means and How to Improve It first appeared on CoolCredit.